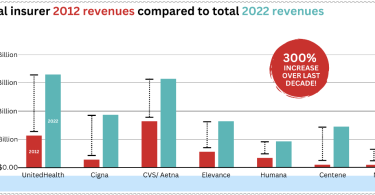

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare...

Big Insurance revenues and profits have increased by 300% and 287% respectively since 2012 due to explosive growth in the companies’ pharmacy benefit management (PBM) businesses and the Medicare...

In a move generally ignored by most media outlets, the Biden administration this week made the shareholders of a small number of for-profit health insurers much richer. As I’ve noted many times in...

When I was a health insurance communications exec, I was a big part of an ongoing effort–funded by your premium dollars–to get you to believe big myths about the U.S. healthcare system. Even a...

Note: This post was originally published on The Potter Report. Congrats, America! Earlier this month you passed an annual milestone: Two days after Tax Day, you made it to… Deductible Relief...

As millions of Americans celebrated President Biden’s inauguration, some of my former colleagues in the health insurance industry were quietly celebrating some news of their own: their most...

The U.S. Department of Justice is trying to block Aetna’s merger with Humana. And, Aetna, along with other for-profit insurers, are pulling out of most of the Obamacare state exchanges...

What can be done to reduce the outsized influence of special interests and a handful of billionaires on our political system? My new book with Nick Penniman, Nation on the Take: How Big Money...

What can we do to fix our democracy? We need to be out there advocating for reform. Among other things, we need to get big money out of politics and health care. It’s corrosive. In Deadly...

Arguably, the people who have benefited most from the health care law—at least financially—are the top executives and shareholders of the country’s health insurance companies. And to maximize...