Access

Medicare Annual Open Enrollment: Beware of Bad Actors ...

Americans want health care system overhaul

Ten ways to improve Medicare Advantage

Four things to think about when choosing between...

Costs in Medicare Advantage present barrier to care

Coronavirus: How many Medicare Advantage members went...

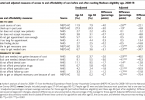

Access to affordable care improves when people enroll...

People with low incomes struggle to access care in US