Costs

States address prior authorization denials, while...

Medicare Part D drug coverage stunts are rampant

Medicare Part D plans can make it hard to get...

Poll: Health care concerns rank high, embedded in...

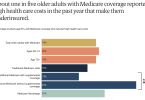

People with Medicare spend twice as much on healthcare...

Poll: Health care costs are a top economic priority...

People in Medicare Advantage struggle to afford their...

Blue Shield of California ends contract with CVS...