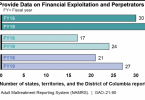

Data

How Connecticut Eliminated Capitated Managed Care in...

Coronavirus: What to think about Omicron

Insurers use prior authorization to keep people from...

Expanding Medicare Advantage is a bad idea

Coronavirus: Senator Casey proposes legislation to...

We pay a lot more than we realize for prescription...

Health care: Where’s the data?

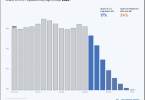

Debt among older Americans increasing in good part...