Income

Health care costs are prohibitive for one in three...

Do you qualify for hospital charity care?

People with low incomes struggle to access care in US

Medicare for All lowers taxes for most Americans

Top Social Security questions and answers

Congress may end tax deduction for medical expenses

Health care has become increasingly unaffordable

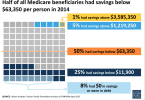

2014 data on income and savings of people with Medicare