Medicare Part D

Medicare Part D in 2018

Out-of-pocket costs for Part D generics way up

Trump shows his support for big Pharma

CVS Caremark accused of $1 billion in Medicare drug...

Budget deal lowers drug costs for people with Medicare

Medicare Advantage: Disenroll between January 1 and...

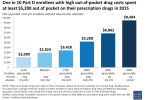

Medicare drug benefit leaves many with high...

Will CMS reduce people’s Part D drug costs?