Quality

Poll: What do Americans think about their health care?

2025: Will Congress extend Medicare telehealth...

Poll: Few Americans are happy with health care quality

2023: Five things to think about when choosing between...

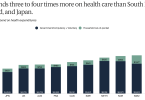

US continues to spend more for poorer quality care...

Medicare Advantage plans fail to release data required...

Data show Medicare Advantage covers less nursing...

Paying more for a Medicare Advantage plan is likely a...