Sarah Kliff reports for the New York Times that labs around the country are charging wildly varying...

Sarah Kliff reports for the New York Times that labs around the country are charging wildly varying...

A new paper by Steffie Woolhandler et al. in the Annals of Medicine exposes our health care...

If you’re looking for free local resources to help older adults, your local Area Agency on Aging...

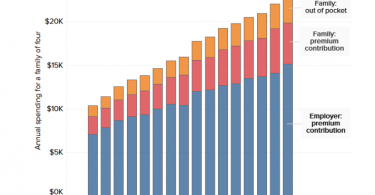

Because health insurance no longer covers large portions of people’s health care costs...

Americans want Congress to address out-of-control health care costs; these costs have been...

If you have Medicaid or can afford supplemental coverage to fill gaps in traditional Medicare...

In a Washington Post op-ed, William E. Bennett Jr., a gastroenterologist and associate professor of...

Kaiser Health News reports that people with the wherewithal to shop around for affordable health...

The Center for Retirement Research blog focuses on how health care information tends to confuse...

Not long ago, advocacy groups called out the Centers for Medicare and Medicaid Services (CMS) for...