The Program of All-inclusive Care for the Elderly (PACE) is a home and community-based program...

The Program of All-inclusive Care for the Elderly (PACE) is a home and community-based program...

Medicare only covers about half of a typical person’s health care costs, leaving people with...

Medicare’s Program of All-inclusive Care for the Elderly or PACE has been a godsend for a small...

Jay Caspian Kang writes about Covid-19 and the nursing home tragedy in the US in an opinion piece...

Medicare only covers about half of a typical person’s health care costs. So, even with Medicare...

Daryl Austin writes for Kaiser Health News about dental fraud. Yes, dentists sometimes identify...

For all the tragedy that Covid-19 has wreaked on this nation, there are a few silver linings...

Since the start of the novel coronavirus pandemic, more than 46,000 people have died in nursing...

A story in The Guardian about corporate entities that buy up nursing homes, with the goal of...

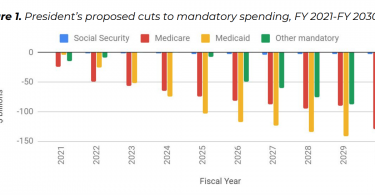

Monique Morrissey writes for the EPI blog about President Trump’s proposed 2021...