In January 2017, the Centers for Medicare and Medicaid Services, CMS, will launch a new initiative...

In January 2017, the Centers for Medicare and Medicaid Services, CMS, will launch a new initiative...

Telehealth or telemedicine–the provision of care through telephone or digitally, including...

It has been the norm that when people first go on Medicare, they are automatically enrolled into...

When it’s time to sign up for Medicare, information can be confusing. Before enrolling in...

Uwe Reinhardt, PhD, writes Why Many Medicare Beneficiaries Cling to an Allegedly Worse Deal in JAMA...

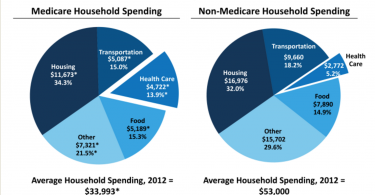

One fourth or so of Medicare annual spending–about $33,500 a person–goes to the cost of...

Until recently, the Medicare Part B premium (medical insurance) was the same for everyone...

There are reasons you should not trust your health plan’s provider directory, and you can...

Many people do not realize that health care costs are almost 14% of household income for people...

If you’re struggling to choose a health plan that’s “right for you,” you’re in...