Uwe Reinhardt, PhD, writes Why Many Medicare Beneficiaries Cling to an Allegedly Worse Deal in JAMA...

Uwe Reinhardt, PhD, writes Why Many Medicare Beneficiaries Cling to an Allegedly Worse Deal in JAMA...

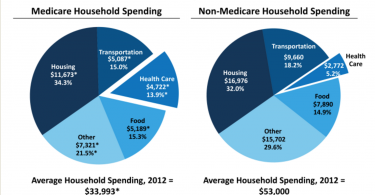

One fourth or so of Medicare annual spending–about $33,500 a person–goes to the cost of...

Until recently, the Medicare Part B premium (medical insurance) was the same for everyone...

There are reasons you should not trust your health plan’s provider directory, and you can...

Many people do not realize that health care costs are almost 14% of household income for people...

If you’re struggling to choose a health plan that’s “right for you,” you’re in...

These days, choosing a health plan that saves you money is a bit like throwing a dart. If you...

It was a balmy fall day last year, when I walked through the surprisingly creaky door of a...

Depression can be crippling, disrupting people’s daily lives and normal functioning. But it...

One of the biggest problems with health insurance companies is that they generally offer health...