The buzz for boomers & carers

What’s Buzzing

Health and financial security

Drugs and technology

Long-term care

Medicaid

Medicare

Social Security

Your Health & Wellness

Drugs and alcohol

Health conditions

Living well

Preventive care

Supplements

Your Coverage Options

Health conditions

Health insurance

Long-term care

Medicaid

Medicare

Pensions

Advice A to Z

More…

About

Get Help

Subscribe

Get Nostalgic

Authors

Team

Contact Us

Terms Of Use

Privacy Policy

Assets

Health and financial security

•

What's Buzzing

Health care costs are prohibitive for one in three...

Social Security

•

What's Buzzing

Is it fair to say we have a retirement crisis?

Health and financial security

•

What's Buzzing

MyRA, a new retirement savings option from the U.S...

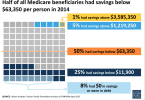

Medicare

•

What's Buzzing

2014 data on income and savings of people with Medicare

Health and financial security

•

What's Buzzing

Income and assets of people with Medicare: Kaiser...

The buzz for boomers & carers

The buzz for boomers & carers