Health and financial security • What's Buzzing For-profit hospitals are causing rising medical debt...

Health and financial security • Medicare • What's Buzzing Berwick: Medicare for All lowers costs and reduces...

Medicare • Social Security • Social Security • What's Buzzing • Your Coverage Options Social Security benefits will rise 2.8 percent in...

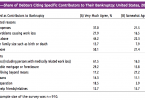

Health and financial security • What's Buzzing To reduce risk of bankruptcy, plan ahead for retirement

The buzz for boomers & carers

The buzz for boomers & carers