Deductible

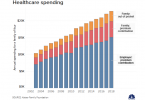

Health care costs continue to rise faster than...

What are Medicare premium and other costs in 2020?

Ten ways Medicare Advantage plans differ from...

Health care information confuses people

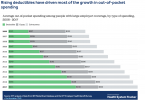

Health insurance deductibles continue to rise

Medicare Medical Savings Accounts could cost you...

Congresswoman Jayapal introduces Medicare for All bill

Eve’s story: Commercial health insurance...