Extra Help

Six tips for keeping your drug costs down if you have...

2022: Programs that lower your health care costs if...

2021: Programs that lower your health care costs if...

Medicare Part D drug coverage in 2021

Medicare Part D drug coverage in 2020

Programs that lower your costs if you have Medicare

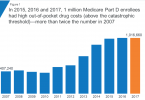

Prescription drug costs soar for people with Medicare...

Medicare Part D drug coverage