GAO

Government watchdog agencies tell Congress Medicare...

High proportion of people flee Medicare Advantage at...

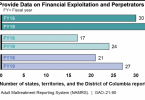

Who’s protecting older adults from financial...

Major problems with Medicare Plan Finder

Congress should level the playing field between...

Medicare Advantage plan “honor system” can...

Avoid memory supplements

Are commercial Medicaid and Medicare plans a good...