Health insurance

How big insurers please Wall Street’s investors

Does your Medicare Advantage plan deny care...

Will Kaiser Permanente’s purchase of Geisinger...

Health insurers increasingly deny coverage for...

Who’s enrolling in Medicare Special Needs Plans?

Big insurer earnings total $1.25 trillion in 2022

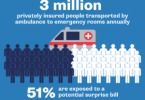

When will Congress address surprise ambulance bills?

HCA hospital system is charged with overtreating...