Social Security 2100 Act

Health care costs eat into your 2021 Social Security...

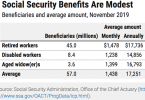

Social Security benefits are relatively small

Top Democratic presidential candidates support...

2020 Social Security benefits should rise, but checks...

Top Social Security questions and answers

The fight to strengthen Social Security is about...