Elisabeth Rosenthal reports for The Washington Post on a patient with psoriatic arthritis who was...

Elisabeth Rosenthal reports for The Washington Post on a patient with psoriatic arthritis who was...

GLP-1 drugs, like Wegovy, Ozempic and Zepbound, are helping millions of Americans lose weight. At...

Medicare for those who choose it–public health insurance–would lower people’s health...

One big insurer, Anthem, denied coverage inappropriately to a woman who needed medicine to ward off...

Max Blau reports for Pro Publica on how the big insurers provide their enrollees with misleading...

If you’re wondering why insurance companies deny necessary care and get away with it...

Americans are finding it increasingly difficult to meet their and their loved ones’ long-term...

Aaron Carroll writes for the New York Times about how to fix our broken health care...

I promoted Mark Cuban’s Cost Plus Drugs a while back as a way to get low-cost generics. As it...

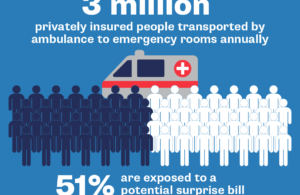

Surprise medical bills are all too common, leaving millions of Americans with health care costs...