Medical debt

Why can’t people know their health care costs...

New bill in Congress would cancel medical debt

Hospital billing practices frequently leave people...

Older adults owe $54 billion in medical debt

Medical debt is a profit center for banks and private...

2022: Health care costs threaten the well-being of...

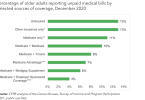

Medical debt more prevalent among Medicare Advantage...

Avoid a lawsuit, don’t sign nursing home...