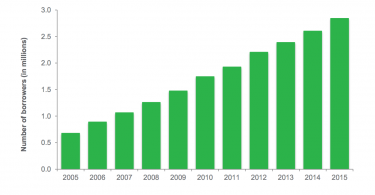

A new report from the Consumer Financial Protection Bureau (CFPB) reveals that nearly three million...

A new report from the Consumer Financial Protection Bureau (CFPB) reveals that nearly three million...

These days, it can be hard to find issues upon which the overwhelming majority of people in the...

Social Security just announced the cost-of-living adjustment, COLA, for Social Security, and the...

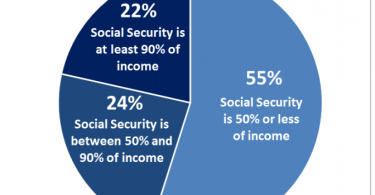

Of all the federal government programs in the U.S., Social Security is perhaps the most...

Back in June, I reported for Just Care that Congress was keeping the Social Security Administration...

On September 9, U.S. Representatives Linda Sanchez and Mike Honda of California introduced...

Daniel Marans writes for the Huffington Post about Social Security’s 81-year impact. From its...

In sharp contrast to the 2016 Republican Party platform, the Democratic Party platform proposes to...

Trump has not spent much time talking about his vision for Social Security, Medicare and health...

Social Security is our nation’s premiere social insurance program promoting security for roughly...