As a result of inflation, people on fixed incomes find that their incomes decline in value over...

As a result of inflation, people on fixed incomes find that their incomes decline in value over...

The Pew Charitable Trust released a report explaining how to maximize Social Security benefits. The...

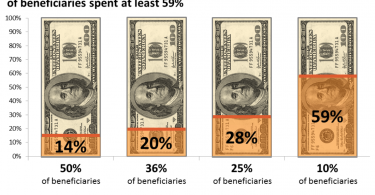

Medicare works to ensure people access to quality affordable health care, but average out-of-pocket...

One of the strengths of Social Security is that benefits are adjusted annually to offset increases...

When deciding when to stop working and when to claim Social Security benefits, there is a lot to...

About 10 million people qualify for Social Security and Medicare on the basis of a disability. ...