What will your Social Security benefit be when you retire? Knowing how much you will receive from...

What will your Social Security benefit be when you retire? Knowing how much you will receive from...

You have earned your Social Security benefits. You should claim them when it meets your personal...

On August 14th, 1935, President Franklin D. Roosevelt signed Social Security into law. Eighty-eight...

Mark Miller writes for his subscription blog, RetirementRevised.com on how cost of living...

On this 19th anniversary of the horrific attacks of September 11, 2001, we find ourselves in the...

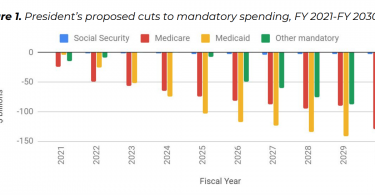

Monique Morrissey writes for the EPI blog about President Trump’s proposed 2021...

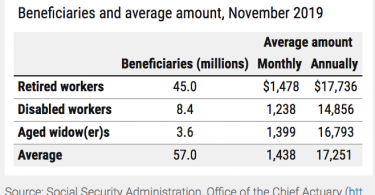

Most people get Medicare just before they turn 65 (though people with disabilities get Medicare...

As often as they can, Republicans in Congress argue to “reform” Social Security...

The New York Times answered the top Social Security questions from its readers. Question 1. Is...

Bloomberg News reports that Americans lose trillions of dollars because they do not claim Social...